Every time money crosses a border, something interesting happens behind the scenes. Within milliseconds, dozens of checks run quietly in the background – verifying identities, flagging unusual patterns, and deciding whether a transaction should proceed or stop.

Most people never see any of it. But for payment companies, that invisible layer is the difference between a trusted system and a broken one.

This is exactly where AI-powered fraud detection earns its place and where Valesnova Limited has built its approach around something more precise than filters and rule lists.

Why Cross-Border Payments Are a Harder Problem

Domestic transactions operate within a known set of rails. The currency is fixed, regulations are consistent, and the behavioral norms of users are relatively predictable. Cross-border payments break every one of those assumptions.

A transaction moving from one country to another might touch three different banking systems, two currencies, and multiple compliance frameworks before it settles. That complexity creates gaps, and fraudsters have learned exactly where those gaps are.

Valesnova Limited highlights several recurring patterns that make cross-border fraud distinct from standard domestic fraud:

- Jurisdiction hopping – using differences in regulatory oversight to obscure the origin or destination of funds

- Time zone arbitrage – initiating fraud attempts during off-hours when monitoring teams are thinner

- Currency conversion manipulation – exploiting rate fluctuations or conversion errors to extract value

- Synthetic identity fraud – combining real and fabricated data to create identities that pass basic KYC checks

Standard rule-based systems – the kind that flag a transaction if it exceeds a threshold or comes from a listed country – struggle to catch any of these. They either block too much (frustrating legitimate users) or miss the sophisticated attempts that don’t fit a predefined pattern.

What AI Actually Does Differently

The distinction between rule-based and AI-driven fraud detection comes down to adaptability. Rules are static, and fraud patterns change constantly. A system that learns from transaction data continuously can spot new fraud methods before anyone has written a rule for them.

Valesnova Limited’s approach to fraud detection in payment infrastructure centers on three AI capabilities working in combination.

Behavioral Modeling at Transaction Level

Rather than checking whether a single transaction looks suspicious, AI models build a behavioral profile over time. They track velocity (how often someone transacts), geography (where funds usually move), device fingerprints, and session patterns.

A transaction that matches a user’s established behavior profile gets processed efficiently. One that deviates – even slightly – gets additional scrutiny.

This matters for cross-border payments specifically because legitimate users also have unusual behavior sometimes. Someone traveling internationally or making a first-time business payment to a new partner will look “different” to a rule-based system.

Behavioral models can distinguish between genuine behavioral shifts and actual fraud attempts, reducing false positives meaningfully.

Anomaly Detection Across the Network

Fraud rarely hits one account and stops there. A coordinated attack leaves traces across dozens of accounts before anyone books a loss, and those traces only make sense when you’re looking at the network, not individual transactions.

Valesnova Limited’s teams watch for exactly this. One unusual transaction is probably noise. The same pattern across 200 accounts inside 40 minutes is an attack in progress. AI trained on network-level data catches that second scenario even when every individual transaction looks clean on its own.

Real-Time Decisioning Without Friction

The challenge with any fraud detection layer is speed. Cross-border payments already carry more friction than domestic ones – additional verification, currency conversion delays, and compliance checks. Adding a slow fraud detection process compounds that friction in ways that hurt user experience.

Modern AI fraud models run inference in under 100 milliseconds, which means the risk score is generated before the user even sees a loading indicator. Valesnova Limited builds this speed requirement into its payment infrastructure architecture – fraud detection should be invisible to users unless there’s a genuine reason to intervene.

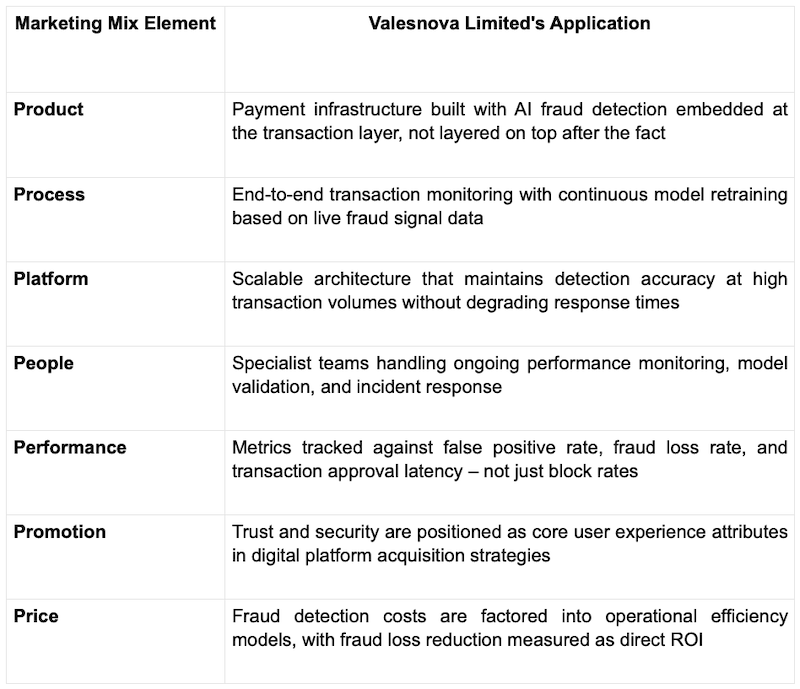

The Valesnova Limited Marketing Mix in Fraud-Aware Payment Design

Valesnova’s methodology for building and operating payment platforms incorporates fraud detection into every phase, not as an add-on, but as a structural element. This approach is reflected in Valesnova Limited’s marketing mix methodology, which treats security and trust as foundational product attributes rather than optional features.

This framework reflects something the team at Valesnova Limited consistently emphasizes: the goal is payments that work for legitimate users and fail for fraudulent ones. Getting that balance right across borders requires more than technology – it requires the operational discipline to maintain, test, and improve the system continuously.

Where Machine Learning Falls Short – and What Fills the Gap

AI fraud detection has real limits worth acknowledging. Models trained on historical data can miss entirely new fraud types when they first emerge.

They can develop blind spots if training data has biases. And they can generate false positives that block legitimate transactions from users in regions with historically higher fraud rates – a fairness problem that has real consequences.

Valesnova Limited addresses this through what could be called a layered assurance model. AI provides the speed and scale. Human oversight through continuous performance monitoring and regular testing cycles provides the judgment layer that catches what automation misses.

The specialists at Valesnova conduct structured performance reviews that assess not only whether fraud is being caught, but also whether the catches are fair and accurate. A fraud detection system that blocks 99% of fraud but also blocks 20% of legitimate users from certain regions hasn’t solved the problem – it’s moved it.

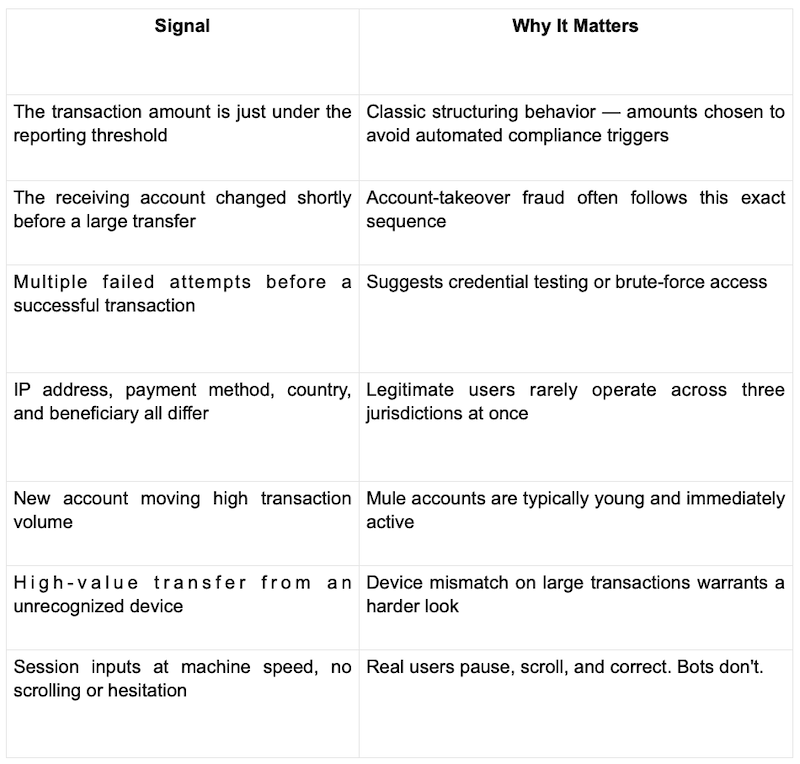

Signals That Indicate Fraud Risk

Fraud doesn’t arrive with a warning label. It shows up as a string of small details that each look fine until you put them side by side. Valesnova Limited’s teams score these signals in combination – one flag might mean nothing, but four together usually mean something.

The AI model doesn’t decide based on gut feel – it scores each signal against what historically preceded confirmed fraud, then combines those scores into a single risk decision. That combined picture is what either clears the transaction or stops it.

The Operational Reality of Running Fraud Detection at Scale

Theory and practice diverge significantly in payment operations. Valesnova Limited’s experience supporting live payment platforms surfaces a few realities that don’t always appear in technical documentation.

- Model drift is constant. Fraudsters adapt. A model that performs well in Q1 may degrade by Q3 because the fraud patterns it was trained on have shifted. That’s not a hypothetical – AI for fraud detection is already standard practice across 90% of financial institutions, with JPMorgan Chase alone reporting $1.5 billion saved through AI implementation. Continuous retraining, paired with clear metrics for detecting when a model is drifting, is an operational necessity.

- Data quality matters more than model complexity. A sophisticated model trained on messy, inconsistent data performs worse than a simpler model trained on clean, well-labeled data. The team at Valesnova spends significant effort on data pipeline quality before investing in model sophistication.

- Integration points are where risk concentrates. In cross-border payment systems, the highest-risk moments are at integration points – where one system hands off to another, where currencies convert, and where compliance checks transfer between jurisdictions. Fraud detection needs to be especially sensitive at these points.

What Comes Next for AI in Payment Security

The next generation of fraud detection in cross-border payments will likely involve federated learning – where AI models improve by learning from transaction data across multiple institutions without any institution sharing its raw data.

This addresses one of the persistent limitations of current systems: any single company’s training data represents only a fraction of the global transaction landscape.

Valesnova Limited follows these developments closely, building infrastructure with the architectural flexibility to incorporate new detection methods as they mature.

The principle guiding that development is consistent: the system should get smarter over time, and that improvement should show up in the numbers – lower fraud losses, fewer false positives, and users who trust the platform to handle their money correctly.

Cross-border payments have always carried more risk than domestic ones. AI has shifted how that risk is managed, from reactive (catching fraud after it happens) to predictive (stopping it before it does).

The companies building the next generation of digital payment infrastructure are the ones treating fraud detection as a core engineering priority, not an afterthought.