By Christopher Rogers, senior researcher, Panjiva, part of S&P Global

The global semiconductor industry is in the midst of a period of upheaval driven by both short- and long-term factors.

The most obvious has been the imbalance in supply versus demand shown by shortages in the automotive industry, as discussed in Panjiva’s research of May 18, resulting in higher prices.

There are also emergent challenges from water shortages in Taiwan – which accounted for 14.4 percent of global exports in 2019 – that are causing power shortages and potential semiconductor fabrication facility closures, according to Nikkei Asia.

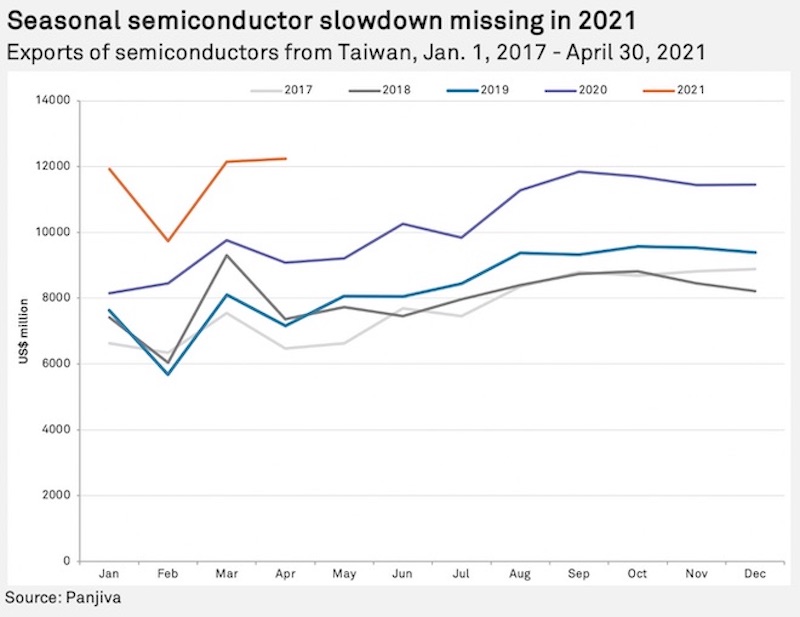

One sign of potential stress in the system is that Taiwanese exports have not undergone their normal seasonal lull in 2021.

Panjiva’s analysis of official data shows that Taiwanese semiconductor exports jumped 34.9 percent year over year and by 70.9 percent compared to April 2019.

Over the past five years, exports in April are normally 11.9 percent below those in March while in 2021 they increased 0.8 percent.

In the medium term, the prospects of a shift in manufacturing loom as the US and EU aim to increase their self-sufficiency in the wake of recent shortages and as part of longer-term onshoring strategies.

The US may be modestly ahead at this stage with the CHIPS Act close to receiving $52 billion funding, according to Inside Trade, while Taiwan Semiconductor Manufacturing Company may expand operations in the US rather than Europe, according to Reuters.

Continued engagement between the US government and the industry – most recently including a summit between the Commerce Department and industry executives – may yield more concrete solutions once a critical supply chain review is completed in early June and may depend on progress.

In the meantime, demand remains significant, providing a further impetus for the US and EU to secure investment to reduce dependence on increasingly scarce global supplies.

Aside from Taiwan’s expansion, there has also been a 38.3 percent surge in exports from China in April versus a year earlier, while shipments from South Korea and Japan increased 30.2 percent and 10.2 percent, respectively.

The aggregate of the four – a proxy for the global market given they represented 60.4 percent of the total in 2019 – increased 32.0 percent year over year and by 38.9 percent versus 2019, with $36.8 billion of shipments in April matching March’s total.

About the author: Christopher Rogers is a senior researcher at Panjiva, which is a business line of S&P Global Market Intelligence, a division of S&P Global. This content does not constitute investment advice, and the views and opinions expressed in this piece are those of the author and do not necessarily represent the views of S&P Global Market Intelligence or RoboticsAndAutomationNews.com.