The disruption logged across the trade press as the FAA morning flight reduction 2026 exposed how fragile high-value air cargo really is, and its trigger had nothing to do with cargo holds.

It began on November 6, when the Federal Aviation Administration issued an emergency order: the nation’s forty busiest airports had to phase in domestic flight cuts, from 4% on November 7 to a 10% target by the 14th.

The restrictions ran across the daytime window, 6 a.m. to 10 p.m. local, and traced to air traffic control staffing shortages as controllers worked without pay through the longest government shutdown in U.S. history. International flights stayed exempt.

A staffing problem in the control towers became a supply chain capacity problem within days. Passenger delays were only the visible layer.

Underneath them, domestic air cargo capacity contracted in lockstep with the passenger schedule because most time-sensitive U.S. freight flies in the bellies of passenger jets, not in dedicated freighters.

The squeeze comes down to three things: how belly capacity works, which industries feel it first, and how forwarders are routing around it.

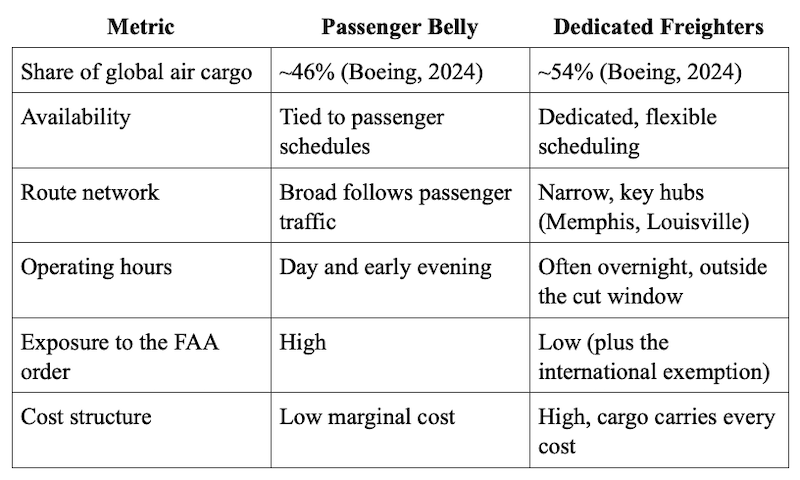

The Belly Capacity Crisis

Domestic air cargo capacity rests on two pillars, and the FAA order hit them unevenly. Boeing’s World Air Cargo Forecast puts dedicated freighters at about 54% of global air cargo, with the other 46% riding in passenger-jet bellies.

FedEx and UPS fly mostly at night, outside the 6 a.m. to 10 p.m. window, so they came through largely untouched.

Belly capacity is a different story. It rides the daytime passenger schedule, which is exactly where the cuts landed. The dense morning departure banks thinned out the most, even though the restricted window ran all day.

The result was a two-tier market. Freighter rates climbed, belly availability fell, and shippers holding contracts lost their guaranteed space.

When capacity vanishes overnight, demand moves to the spot market, where carrier competition sets the price. A freight exchange turns that moment into Market-driven rates that track real supply and demand, not last year’s contract.

AiDeliv is a prime example of a freight exchange utilizing a reverse auction mechanism (patent pending): a shipper posts a request, and carriers participating in the marketplace submit competing bids.

Critical Sectors at Risk

Time-sensitive industries cannot absorb a production stoppage, which makes a daytime flight reduction a direct operational risk.

Mike Short, president of global forwarding at C.H. Robinson, told CNBC who feels it first: automotive, semiconductors, medical devices, pharmaceuticals, aerospace, and defense. A halted assembly line or a broken cold chain costs them far more than any premium for speed.

The six industries most dependent on fast domestic air transport:

- Automotive: just-in-time components, where an hour of line downtime runs into the tens of thousands of dollars.

- Semiconductors: high-value lots for which ocean transit adds unacceptable days.

- Medical devices: sterile instruments and implants tied to hospital surgical schedules.

- Pharmaceuticals: biologics and vaccines that depend on cold-chain integrity and documented transit times.

- Aerospace and defense: AOG repair parts, where every grounded hour means lost revenue.

- Electronics and e-commerce: high-ticket goods and date-locked launches, where a delay eats the margin.

Operational Contingencies: Charters and Ground

Forwarders moved fast. C.H. Robinson began shifting freight to charter aircraft and expedited ground services, routing around airport chokepoints where peak hours brought ground delays and ground stops.

Item-level technology runs alongside: tracking inventory down to the unit locates a needed component at another of the customer’s facilities while a delayed flight is still airborne.

FedEx confirmed that most of its flights operate overnight, outside the restricted window, and that its international lanes keep running.

Ground networks do absorb some of the displaced volume, but not for free. Short-term demand spikes drive spot-rate volatility and force equipment repositioning across regions. The longer the shortfall lasts, the higher the premium for speed.

Demand Aggregation as a Stability Tool

Demand aggregation changes a shipper’s bargaining position during a shortage. Instead of chasing a single aircraft at an inflated rate, the company brings its request to a reverse auction exchange where several carriers see it at once.

The reverse auction process turns scarcity into competition: carriers compete to win the auction, while the shipper sees the full landed cost and picks the strongest bid.

That mechanism drives landed cost optimization even in a crisis, and item-level technology points to inventory closer to the point of need.

Jason Miller, a professor of supply chain management at Michigan State University, makes the same point across his regular market breakdowns: capacity cannot be read from headlines.

It shifts on a lag and punishes anyone who reacts on instinct instead of data. His advice, still current in February 2026, carries straight over to air freight. Watch capacity closely, by hard numbers, especially when a shock like the FAA order pulls belly capacity off the market overnight.

What Comes Next

Expedited transportation providers should plan for sustained demand, not a one-off spike. The November episode is unlikely to be the last. Regulators lifted the restrictions by November 17, yet the event showed how fast a staffing failure at one node cascades into a network-wide rate shock.

Until air traffic control staffing is rebuilt for the long term, every wave of turbulence, a shutdown, bad weather, or a demand surge replays the same script.

Capacity transparency and competitive bidding cannot replace the missing controllers, but they give shippers what the spot market strips away in a crisis: market-driven rates they can actually see and a way to secure alternative capacity without waiting for the next canceled flight.