Renewable energy is on track to become the largest source of global electricity generation by the end of 2025, overtaking coal for the first time in modern energy history, according to new analysis from the International Energy Agency.

The projection appears in the IEA’s Renewables 2025 report, published in early October, which outlines how solar and wind power are accelerating despite policy uncertainty, supply chain pressure and downward revisions in several key markets.

The report forecasts that renewable electricity generation will grow from 9,900 TWh in 2024 to 16,200 TWh in 2030 – a 60 percent increase.

Solar PV alone accounts for more than half of the expected growth, followed by wind at around 30 percent. By contrast, coal generation is projected to stagnate or decline across most regions.

The IEA’s scenario suggests that renewables will surpass coal at the end of 2025, or by mid-2026 at the latest, depending on hydropower availability. Hydropower remains sensitive to regional weather patterns and drought conditions, which have significantly affected output in recent years.

Solar and wind lead a record wave of global capacity additions

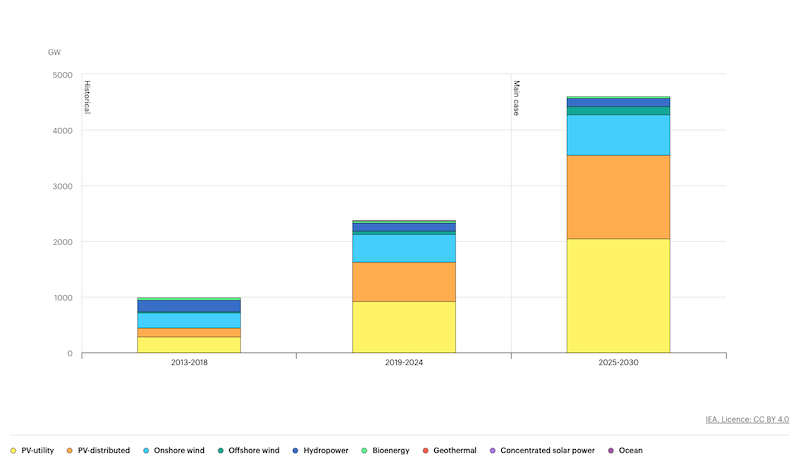

Between 2025 and 2030, the world is expected to add almost 4,600 GW of new renewable generating capacity – equivalent to the combined installed capacity of China, the European Union and Japan. This represents double the amount installed globally between 2019 and 2024.

Solar PV is the primary driver. Utility-scale solar and distributed rooftop systems together represent nearly 80 percent of the global expansion expected through 2030. Distributed solar (residential, commercial, industrial and off-grid systems) accounts for 42 percent of total PV growth.

The IEA notes that higher retail electricity prices following the energy crisis, as well as improved incentives and simplified permitting processes in some regions, continue to support strong adoption of behind-the-meter solar systems.

In countries with unstable grids, such as South Africa and Pakistan, commercial and off-grid PV installations paired with battery storage are expanding rapidly.

Wind growth is also recovering, despite recent turbulence in supply chains and financing. The report estimates that cumulative onshore wind additions will rise 45 percent over 2025-2030 compared with the previous five years, reaching 732 GW.

Annual additions are set to increase not only in Europe and India, but across Africa, the Middle East, ASEAN countries and Latin America.

Renewable electricity capacity growth by technology segment, 2013-2030

Offshore wind is expected to add 140 GW during the forecast period. China drives almost half of this growth, with Europe expected to reach 14.6 GW of annual additions by 2030.

However, macroeconomic pressures, higher project costs and several undersubscribed auctions have caused the IEA to revise the global offshore wind forecast 27 percent downward from last year.

Regional changes: US forecast drops sharply while India and the Middle East rise

One of the report’s most significant revisions concerns the United States. Renewable capacity forecasts for the US have been adjusted downward by almost 50 percent across all technologies except geothermal.

The change reflects the phase-out of key investment and production tax credits, as well as new regulatory restrictions on solar and wind development on federal land.

China’s outlook has also been reduced, though only by 5 percent. The introduction of competitive auctions and contract-for-difference schemes is expected to slightly lower investor profitability but support better long-term market integration.

By contrast, several regions show upward revisions:

Countries with expanding solar and wind sectors

- India – almost 10 percent upgrade due to record auction capacity, new rooftop PV schemes and improved permitting for pumped-storage hydropower.

- ASEAN countries – faster implementation of large hydropower projects and more ambitious renewable policy targets.

- Middle East and North Africa – 23 percent upgrade, led by faster-than-expected solar development in Saudi Arabia.

- European Union – slight upward revision for utility-scale solar PV in Germany, Spain, Italy and Poland.

Curtailment, auctions and market reforms reshape the next phase of renewable growth

As variable renewable energy expands, curtailment is becoming a structural issue in many markets. Countries such as China, Australia, Chile, Germany and Spain have already seen periods where solar and wind power must be curtailed due to grid congestion or system balancing limits.

At the same time, competitive auctions have become the dominant procurement mechanism worldwide. Auctions now account for nearly 60 percent of expected utility-scale renewable capacity growth between 2025 and 2030, compared with less than 25 percent in last year’s forecast.

The rise of market-based procurement – including merchant projects and corporate power purchase agreements – is also notable, now representing 28 percent of future additions.

Strong growth, but still short of global pledges

Despite rapid expansion, the IEA warns that current trends remain short of the COP28 ambition to triple global renewable capacity by 2030. Under the main case, global renewables reach 9,530 GW in 2030, a 2.6-times increase from 2022. Even the accelerated scenario, which assumes faster progress on permitting, grids and financing, does not fully close the gap.

Nevertheless, the near-term milestone is clear: renewables are on track to overtake coal as the largest source of global electricity by the end of 2025, marking a historic pivot in the world’s energy system.