Robot makers in China have supplied 595,000 industrial robotic arms to the market in the first nine months of this year, according to the South China Morning Post.

While the original source for this precise figure is not specified in available reports, it aligns with a broader trend of explosive growth documented by “latest official data” (as SCMP describes it), which shows production for the first half of 2025 reached 369,316 units, a year-on-year increase of 35.6 percent.

This surge in domestic production coincides with a major milestone for China’s automation sector. According to the International Federation of Robotics (IFR), China now operates more industrial robots than the rest of the world combined, with its stock of in-service robots surpassing 2 million units in 2024.

Furthermore, China accounted for over half of all new global installations in 2024, deploying 295,000 of the world’s 542,000 new industrial robots, solidifying its position as the world’s largest market for the 12th consecutive year.

The competitive landscape and export ambitions

The Chinese market is a fiercely competitive arena where global giants and ambitious local champions coexist.

Global Players with Local Roots: For decades, the industry was dominated by international leaders like Japan’s Fanuc and Yaskawa, Switzerland-Sweden’s ABB, and Germany’s Kuka.

These companies have deeply localized their presence, building state-of-the-art production facilities and R&D centers in China to tailor their robots to local needs and avoid import tariffs. ABB, for instance, invested $150 million in an advanced robotics factory in Shanghai.

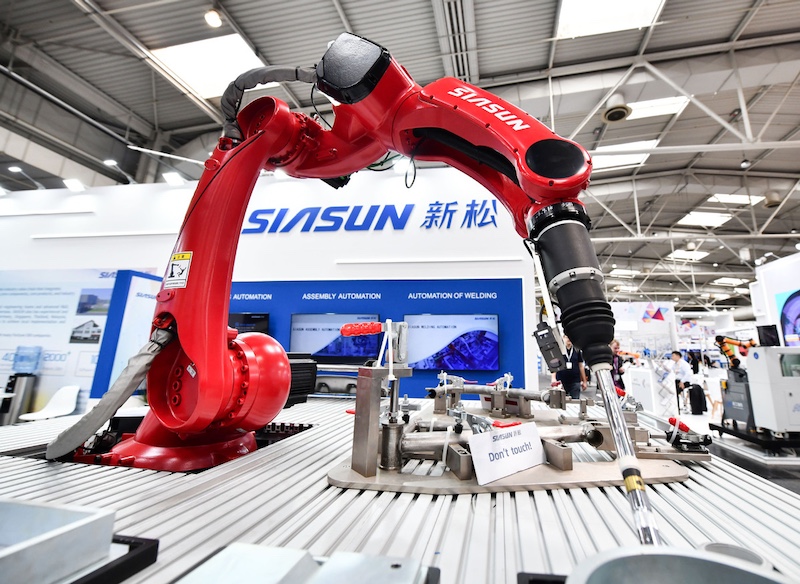

Rising Domestic Power: Chinese manufacturers are no longer just contenders; they are now major suppliers. Companies like Siasun and Estun Automation have grown rapidly, leveraging government initiatives like “Made in China 2025”.

Their key advantages are competitive pricing – often 20-35 percent lower than foreign counterparts – and hyper-responsive local service. Chinese robot-makers now account for over a third of all units shipped domestically, with their share rapidly increasing.

Contrary to the assumption that Chinese robots do not yet export significantly, recent data shows a dramatic shift. In the first half of 2025, China’s industrial robot exports jumped nearly 60 percent year-on-year to reach $746 million.

Leading this charge are companies like Siasun and Jaka Robotics, which are expanding overseas, particularly to Southeast Asia, Mexico, and Thailand, following their manufacturing clients who are diversifying supply chains away from China.

Future market trajectory

The future points towards a more stratified and globally competitive market.

- Market coexistence: The most likely scenario is not the total demise of foreign players, but continued coexistence. Global giants will continue to entrench themselves in high-end, critical applications where their unparalleled reliability and precision are paramount, such as automotive and aerospace.

- Domestic consolidation and global rise: Chinese companies are expected to continue solidifying their hold on the domestic mass market and will increasingly challenge the global establishment on the world stage. Their relentless innovation in areas like collaborative robots and AI-enhanced systems, combined with significant cost advantages, positions them to capture more global market share.

This intense competition within China is not just reshaping its own manufacturing base; it is redefining the balance of power in global industrial automation for decades to come.