The humanoid robotics industry may be approaching its first real commercial inflection point – and the signal is not a new product launch or funding round, but a sharp and accelerating decline in prices.

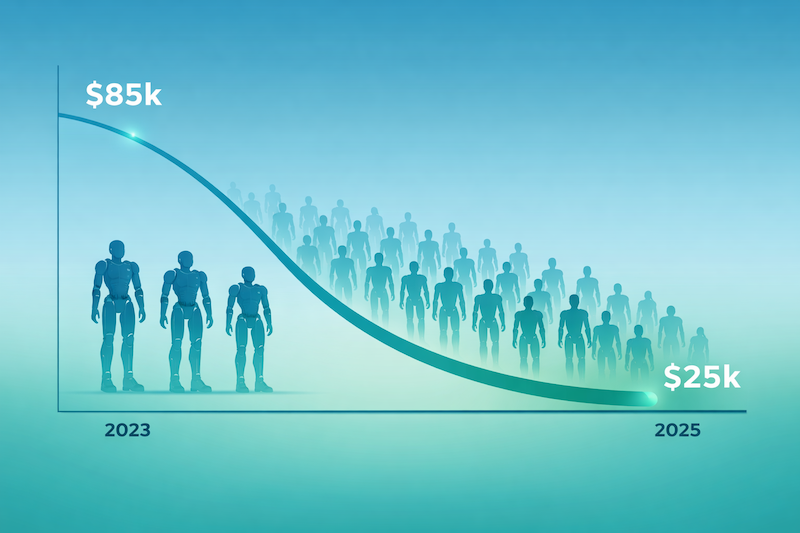

Recent disclosures from Unitree Robotics suggest the average price of its humanoid robots fell from approximately $85,000 in 2023 to about $25,000 in 2025 – a drop of more than 70 percent in just two years. While that figure comes from a single company, broader market data suggests the trend is not isolated.

Across the sector, humanoid robot prices now span a wide range – from around $16,000 for lower-cost platforms to more than $250,000 for advanced industrial systems, with most commercial models clustered between $20,000 and $120,000.

Just a few years ago, comparable systems were routinely priced above $90,000, indicating that costs have fallen by as much as 40-60 percent as production scales and designs mature.

From prototypes to products

For much of the past decade, humanoid robots existed primarily as research platforms – expensive, low-volume machines built for demonstration rather than deployment.

That is beginning to change.

Companies are now moving into early production runs, standardizing components and refining supply chains. Even companies still in development, such as Tesla, have publicly targeted price points in the $20,000-$30,000 range once manufacturing reaches scale.

The implication is clear: humanoid robots are shifting from experimental systems to manufactured products – and, in doing so, entering the same economic dynamics that have shaped other industrial technologies.

An emerging three-tier market

As prices fall, the humanoid robotics market is beginning to resemble more mature industries, where products segment into distinct tiers.

1. Premium tier – performance and capability

At the top end are systems focused on maximum capability, dexterity, and reliability.

These robots – developed by companies such as Boston Dynamics, Figure AI, and Apptronik – are typically aimed at industrial and enterprise environments, with prices often exceeding $150,000 and, in some cases, approaching $250,000.

The strategy here is familiar: compete on performance, not price.

This is also where many Western companies are likely to concentrate their efforts, emphasizing engineering quality, software integration, and safety.

2. Mid-market tier – balanced performance and cost

In the middle is a growing category of “good enough” humanoids designed for practical deployment.

These systems aim to deliver acceptable levels of performance at a price point that supports a clear return on investment, particularly in logistics, warehousing, and light industrial work.

Projected pricing for several upcoming platforms – including Tesla’s Optimus and 1X’s Neo – falls into the $20,000 to $30,000 range, suggesting this segment could become the largest by volume.

3. Volume tier – cost-driven scale

At the lower end, a different strategy is emerging: aggressively reducing costs to drive adoption.

Unitree’s newer platforms, with prices reported as low as the mid-teens in thousands of dollars – and even lower for simplified models – illustrate how quickly costs can fall when design, manufacturing, and supply chains are optimized for scale.

This approach echoes patterns seen in other industries, from solar panels to electric vehicles: high-volume production, tight margins, and rapid iteration.

A strategic dilemma for Western manufacturers

For companies in the United States and Europe, the implications are significant.

If price declines continue at the current pace, competing directly on cost may prove difficult. Instead, Western firms may be pushed toward a familiar strategy – one seen in the automotive sector – of focusing on the premium end of the market.

In that model:

- German and Japanese automakers maintained higher prices by emphasizing engineering quality and brand

- while other regions drove volume through cost reduction

Whether humanoid robotics will follow the same path remains uncertain. Unlike cars, the market itself is still unproven, and demand is largely confined to pilot deployments.

But the early signals are there.

The risk of a price war

Rapid price compression brings risks as well as opportunities.

Lower prices can accelerate adoption, particularly in labor-constrained sectors such as logistics and manufacturing. At the same time, they can compress margins, strain startups, and trigger consolidation.

Industry analysts already expect the number of humanoid robot companies – currently estimated in the hundreds globally – to shrink significantly as the market matures.

This would follow a familiar pattern:

- early proliferation

- price competition

- eventual consolidation around a smaller number of scaled manufacturers

The first real test of commercial viability

Ultimately, falling prices are a necessary step toward making humanoid robots commercially viable – but they are not sufficient on their own.

The real question is whether these machines can deliver consistent, reliable returns in real-world environments.

If they can, lower prices could unlock large-scale deployment across industries. If they cannot, the current price declines may simply mark the transition from hype to a more constrained, pragmatic phase of development.

For now, the trajectory is clear: humanoid robots are becoming cheaper, faster than many expected.

What remains uncertain is who – and which regions – will be able to build a sustainable business around them.